The Four-Layer Structure of New Stagflation: Debt, AI, Quadruple Effects, War

This is a predictive structural analysis—the US has not yet entered formal stagflation (Core CPI ~2.6%, no recession), but structural pressure is accumulating. Should stagflation arrive, most observers will attribute it to war, or believe AI is the disinflationary solution. Both readings would be wrong. The true pathology is a layered structural system—US sovereign debt as the foundation has stripped the system of its braking capacity; AI as the structural transformation engine simultaneously drives up energy demand, structurally absorbs capital, suppresses labor income, and extreme-concentrates wealth and power; war then compresses what would have been 5 years of pressure into 2 years of visibility.

This will not be another business cycle—it will be a wholesale structural transformation.

Four-Layer Structure + Self-Reinforcing Loop

Should new stagflation arrive in the future, today's social tension and geopolitical instability will not be separate problems—they will be four facets of one structure. The foundation is US sovereign debt, which has stripped the system of its braking capacity. The structural transformation engine is AI—it is driving up costs, structurally absorbing capital, suppressing income, and extreme-concentrating wealth and power. The trigger is war, which would compress what would have been 5 years of pressure into 2 years of visibility. The consequence will be that strong nations themselves become structurally unstable internally, while the traditional mechanisms for resisting this structure (democracy, protest, elections) are being simultaneously weakened by AI.

Furthermore—this structure is self-reinforcing. Each layer's outcomes feed back to strengthen the previous layers. Until now, except for physical infrastructure thresholds such as electricity supply and factory capacity (turbines for power plants, equipment for AI data centers), no sufficiently strong natural brake is visible.

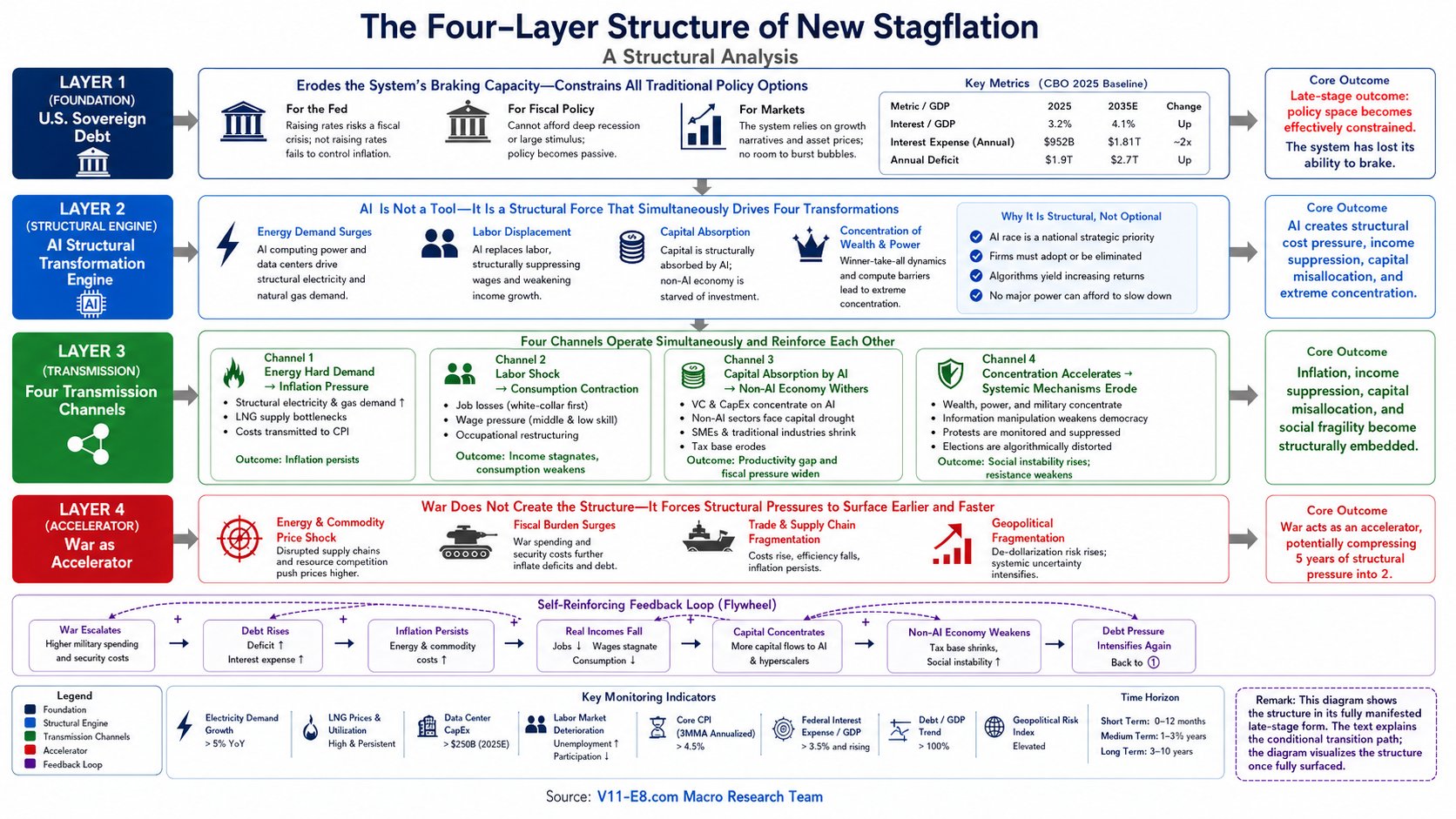

Sovereign Debt (Foundation)

Strips policy braking capacity. Any traditional tool (rate hikes, fiscal tightening, regulation) is constrained by debt burden.

AI Structural Transformation Engine

Not a tool, but a new structural force. Simultaneously drives four structural effects.

Quadruple Effects Transmission

Energy inflation + Labor displacement + Capital absorption + Concentration↔Resistance erosion.

War (Accelerator)

Doesn't create this structure, compresses it from 5 years to 2 years of visibility.

Sovereign Debt—The Foundation That Stripped the System of Brakes.

People typically treat sovereign debt as "another economic problem"—parallel to inflation, unemployment, growth. This reading is wrong. Debt is not one problem among others; it is the structural constraint that makes all other problems unsolvable.

Hard Data: CBO 2025 Projections

| Indicator | 2025 | 2035 (projected) | Change |

|---|---|---|---|

| Debt as % of GDP | 100% | 118% | Rising |

| Interest expense as % of GDP | 3.2% | 4.1% | Rising |

| Annual interest expense | $952B | $1.8T+ | More than doubles |

| Annual deficit | $1.9T | $2.7T | Rising |

Source: Congressional Budget Office, The Budget and Economic Outlook: 2025 to 2035 (January 2025). CRFB Aug-2025 alternative scenario: if 10Y yields stay at 4.3%, +$1.6T over 10 years.

Key observations: Interest expense has exceeded defense spending (~$850B). From 2027 onward, interest expense will exceed all non-defense discretionary spending, and interest as % of GDP will reach the highest level since 1940.

For the Fed / For Fiscal / For Markets

- For the Fed: Rate hikes against inflation trigger fiscal crisis (each 100 bps adds ~$300B annual interest); not raising rates means inability to suppress AI's structural inflation → Fed paralysis

- For fiscal policy: Cannot stimulate during deep recessions; cannot tightly regulate AI either → Policy passivity

- For markets: The entire dollar system depends on growth narrative; once growth expectations collapse, sovereign debt demand collapses; if international parties begin using alternative currencies for settlement, this constitutes a run on the dollar—the US is attempting to use stablecoins to address this crisis (see Series Piece Two, "Stablecoins: A Token from a Private Game Parlor")—but as that piece reveals, this is merely risk reallocation, not actual resolution

This is why Trump is desperately trying to address debt yet faces structural passivity at every turn (see Series Piece One, "Trump's Absolute Passivity"). This piece extends from these two structural observations, revealing the engine driving this structure—AI.

AI is not a tool—it is a new structural force.

The technology revolutions of the past 30 years (IT revolution, internet, smartphones) had an overall disinflationary effect—costs declined, efficiency improved, wages and inflation rose together (productivity gains were broadly shared). The AI revolution has a different structure.

| Dimension | IT Revolution | AI Revolution |

|---|---|---|

| On cost side | Decline (automation lowers cost) | Rising (electricity demand structurally surging) |

| On wage side | Rise (productivity dividends shared) | Declining (direct labor displacement) |

| On capital allocation | Distributed across industries | Highly concentrated (VC 61% to AI) |

| On capital concentration | Moderate (platform economy) | Extreme (winner-take-all + compute thresholds) |

| On overall inflation | Disinflationary | Stagflationary |

AI simultaneously drives four structural effects: pushing up hard energy demand, suppressing labor income, structurally absorbing capital, and extreme-concentrating wealth and power. This is not a difference of degree, but of nature—AI is the first technology revolution to do all four simultaneously.

Why is it a structural force, not a tool?

- Compute competition is nationally strategic—US, China, EU all treat AI as a strategic asset; no nation dares to "stop"

- Corporate competitive pressure—any company that doesn't adopt AI will be eliminated by competitors who do

- Algorithms only accelerate—AI training has increasing returns; better models attract more compute, no natural saturation point

- No policy exit—regulating AI = abandoning competitive position; no strong nation can make this choice

This means AI's structural pressure is unavoidable—unlike the 1973 oil crisis where one could wait for OPEC concession, unlike the 2008 financial crisis where banks could be restructured—it is a permanent structural force.

Four axes operating simultaneously, not sequentially.

Hard Energy Demand → Inflation Pressure

Many believe "recession will lower energy demand." This logic holds for oil. It doesn't hold for electricity.

- IEA: Global data center electricity demand projected at ~460 TWh in 2026, may reach 800-1,000 TWh by 2030 (70-120% growth)

- Plus China electrification, coal retirement, emerging market growth → global electricity demand structurally rising

- Rystad 2026-03: LNG large-frame gas turbines globally supplied by only 3 OEMs, 2-4 year backlog

- Qatar Ras Laffan repair takes 3-5 years—independent of when war ends

Quantitative estimation (BLS weights × historical energy shock elasticity, including 6-12 month lag from physical supply to CPI calculation): Core CPI may rise from 2.6% to 4.78% / 6.03% / 7.26% 12-18 months out (conservative / moderate / aggressive).

Current Core CPI 2.6% reflects pre-war world—BLS calculation of housing (33% of Core) has 12-18 month lag. CPI numbers will continue to look low over the coming year, but this doesn't mean pressure isn't accumulating—it means the dashboard hasn't yet caught up to pressure already in the pot.

Labor Displacement → Consumption Compression

McKinsey 2023-07: "By 2030, up to 30% of work hours in the US could be automated; 12 million career switches required (25% higher than 2021 estimate)."

However, McKinsey's estimate may underestimate—it's built on AI capability assumptions from mid-2023 (around ChatGPT release). Between 2024-2026, multimodal, agent, and reasoning capabilities have all exceeded original expectations. Real effects will scale up dramatically with the exponential improvement of AI capabilities—meaning 12 million career switches may merely be the lower bound.

Even one of the largest AI proponents says the same—Tesla / xAI CEO Elon Musk publicly stated in October 2025: "AI and robots will replace all jobs. Working will be optional" (Musk on X, 2025-10-21). When the AI development community itself publicly acknowledges that "all jobs may eventually be replaced," it means McKinsey's 30% estimate is almost certainly just the lower bound.

Counterintuitive core: GDP can still rise (because AI boosts corporate profit and capital-side returns), but median income falls (because labor side loses bargaining power). Traditional macroeconomic indicators (GDP, total employment) will show "the economy is normal," but the lived experience for individuals is "getting poorer."

Capital Absorbed by AI → Non-AI Economy Desiccated

For the past 30 years, capital markets have been engines of distributed innovation. The AI revolution has changed this structure.

| Year | AI as % of global VC investment |

|---|---|

| 2022 | 30% |

| 2023 | 27.5% |

| 2024 | 40% |

| 2025 | 61% ($258.7B / $427.1B) |

Source: OECD, Venture capital investments in artificial intelligence through 2025 (February 2026). US accounts for 75% of global AI VC ($194B).

Plus Hyperscaler (Microsoft / Google / Meta / Amazon) capital expenditure: 2024 ~$246B → 2025 ~$350-450B → 2026 projected ~$600-700B, with ~75% directly invested in AI infrastructure. Scale equates to 2.2% of US GDP—larger than global solar + wind energy investment combined.

SVB: AI late-stage companies at Series C have a 100% valuation premium relative to non-AI peers—a comparably-sized non-AI company has financing cost more than double that of an AI company.

Structural Consequences (4 chained)

- SME financing structurally difficult—non-AI sectors (80%+ of US employment) bear the greatest squeeze → unemployment pressure rises (strengthening Axis 2)

- Diverse innovation ecosystem structural shrinkage—2025 total VC hits historical highs, but excluding AI ($168.4B), the non-AI portion is below 2022

- Asset pricing structurally distorted—S&P 500 gains highly concentrated in Magnificent 7; bubble risk concentrated in single track

- Tax base structurally weakened—non-AI economy desiccates → tax revenue declines → feeds back to strengthen Layer 1 (debt pressure)

Concentration Acceleration ↔ Resistance Erosion's Mutual Amplification

Axis 4 is not a single mechanism—it's the mutual interaction of two independent mechanisms.

Mechanism One: Concentration Acceleration

- Military concentration (international): autonomous weapons, AI intelligence, precision strike → asymmetric resistance fails

- Wealth concentration (economic): AI revenue highly unequal (downstream consequence of Axis 3)

Mechanism Two: Resistance Erosion

- Democratic mechanisms: effectiveness being diluted by information manipulation

- Protests: capability being suppressed by surveillance and precision crackdown

- Strikes: bargaining power being offset by automation

Creative Planning (managed/advised assets ~$700B) CEO Peter Mallouk (early 2026): "The top 10% of US income earners now account for nearly half of consumption, while the bottom 80% has continued to decline. This is 100% completely unsustainable as a society." What's noteworthy isn't this observation, but who is making it—the CEO of a wealth management firm serving ultra-high-net-worth clients.

Counterintuitive Core: Strong-Nation Internal Structural Instability

Before AI acceleration reaches its peak, the world has already shown signals of structural disorder:

- US: Political polarization, election trust collapse, MAGA, Occupy movement, BLM

- Europe: Yellow Vests, far-right rise, Brexit, energy crisis protests

- China: High youth unemployment, "lying flat" phenomenon, white paper movement

These phenomena have varied causes—some originate in deindustrialization (MAGA), some in policy conflicts (Brexit), some in economic slowdown and social structural pressure (China's "lying flat"), some in the interaction of wealth distribution with social media algorithms (political polarization). They are not all directly caused by AI.

In other words: existing instability is already substantial; but what AI is about to do is a double blow—it expands the audience of instability while stripping away their capacity to fight for themselves.

War would not be the cause—it would be the accelerator that brings forward visibility.

We typically frame war as "the cause of crisis"—this reading would be wrong. War would not create this structure—it would compress what would have been 5-year gradual emergence into 2-year visibility.

| Dimension | Without war | With war |

|---|---|---|

| Inflation visibility timing | 2028-2030 | 2027-2028 |

| Policy response time | Slow but possible | Passive and ineffective |

| Social tension visibility | Gradual accumulation | Rapid emergence |

| Moderate inflation arrival | 2030+ | 2027 H1 |

Without war, this structure would still emerge—just more slowly, and the Fed would still have some adjustment room. With war, the entire process is compressed, and the Fed loses adjustment time. This is the precise meaning of "accelerator."

Why there's insufficient natural brake.

The four layers are not unidirectional causation. They have 6 main feedback lines that make the system self-reinforce.

| Feedback | Origin → End | Mechanism |

|---|---|---|

| R1 | L4 War → L1 Debt | War expenditure, military aid, strategic stockpile → debt rises |

| R3 | L3 Inflation → L1 Debt | Higher rate financing cost → interest expense explodes |

| R4 | L3 Unemployment → L1 Debt | Tax revenue ↓ + welfare ↑ → fiscal worsens |

| R5 | L3 Disorder → L4 War | Strong-nation internal disorder → seeking external outlet |

| R7 | L3 Concentration → L2 AI | Concentrated capital continues to push AI investment |

| R8 | L3 Axis 3 → L3 Axis 4 wealth concentration | Capital allocation distortion → AI revenue accrues to few → strengthens wealth concentration |

This will be a loop where, until now, except for physical infrastructure thresholds such as electricity supply and factory capacity (turbines for power plants, equipment for AI data centers), no sufficiently strong brake is visible—any negative feedback (recession, policy response, social adjustment) would operate at a speed far slower than the positive feedback accumulation, allowing the system to effectively self-accelerate. Each cycle would push the entire system further toward "disorder."

Why this would be harder than the 1970s, should stagflation arrive.

| Dimension | 1970s | 2026+ |

|---|---|---|

| Inflation source | External energy shock (OPEC) | Endogenous AI structure |

| Wage-inflation relationship | Synchronized rise | Inflation ↑ Wages ↓ (AI suppresses wages) |

| Capital allocation | Distributed across industries | AI highly concentrated (VC 61%) |

| Policy space | Volcker could aggressively raise to 20%+ | Debt constrains Fed (rate hikes trigger fiscal crisis) |

| Repair pathway | OPEC could compromise / alternatives | OEM physical limits (2-4 year backlog) |

| Social response | Protests effective | AI surveillance erodes resistance |

| International order | Bipolar relatively stable | AI military exponential gap |

| Common feature | Clear path to resolution | No clear path to resolution |

Across these key dimensions, this stagflation, should it arrive, would be harder to resolve than the 1970s. There would be no Volcker-style move available—rate hikes trigger fiscal crisis, increasing supply is impossible, suppressing demand is impossible (AI structural demand is hard demand), redistribution is impossible (AI concentration is structural).

Three structural orientations for deployers.

This article is not investment advice. But if one accepts the above analysis, several orientations merit consideration.

Orientation One · Liquidity reserves are structurally necessary

- Transmission speed faster than historical experience

- During crisis, liquidity disappears non-linearly

- Leveraged positions get force-liquidated faster than traditional markets

- Holding 15-25% liquidity is the structural necessity for navigating high uncertainty

Orientation Two · Watch the boundary of concentration

- Don't always single-bet on one scenario (over-concentration in AI giants may be policy-reversed at some critical point)

- Don't be overly pessimistic (AI-related investment remains a structural winner short-term)

- Long-term inflation-benefiting real assets (gold, energy, infrastructure, agriculture) are options for resisting economic volatility

- Need to balance hedging with structural exposure

Orientation Three · Replace event prediction with structural observation

Better questions are not "When will the Fed cut rates?" / "When will the war end?" / "When will AI valuations crash?"

But: "Which layer has the structural pressure transmitted to?" / "How fast is the feedback loop accelerating?" / "How effective are resistance mechanisms still?"

This thesis is not faith—it is a structural analysis that can be weakened or revised.

Structural falsifier directions

Undermine Layer 1 / 2 core assumptions

- US debt burden significantly eases (CBO forecast reverses)

- AI trajectory reverses (structural technical bottleneck)

- Resistance mechanisms rebuild (civilizational coordination)

- New disinflationary technology (fusion + cheap storage)

Empirical falsifier directions

Undermine Layer 3 / 4 specific predictions

- Core CPI stays below 3% over the next 2 years

- Median income recovers growth

- Strong-nation internal social stability significantly improves

- Energy prices return to pre-war levels post-war

- AI as % of global VC significantly drops from 61%